What Are The Emotions Of Investing & Do You Have A Financial Plan? - Jaime Gaona

Show original YouTube description

Show transcript [en]

foreign I work at a local Financial firm and Eric I've known Eric for the years and I've been in the betterment village a couple years and he asked if I could do a quick talk about emotions so some of you may or may not know what happened this week but uh the markets actually did me a favor and not a favor so it did me a favor because there is some emotions that come with it it also did not do me a favor because uh my my personal portfolio my client's portfolios are down so it happens the question came up and some research I was doing is should we use emotions in making decisions the answer is yes but you really should

use it as a opportunity to set some guide rails or excuse some guardrails and also set some expectations amongst yourself but you shouldn't Thrive purely on emotional decision so I'm going to jump into it it's only going to be about 10 maybe maybe eight minutes of conversation from me up here but then I'll open it up to questions and answers the one favor I do ask is uh please don't ask any questions specifically about the market I'm here as more of an educational tool and for my compliance Department I'm here is more of having a friendly conversation and not directing you in any Investments or any opportunities you may or may not take fair enough everyone

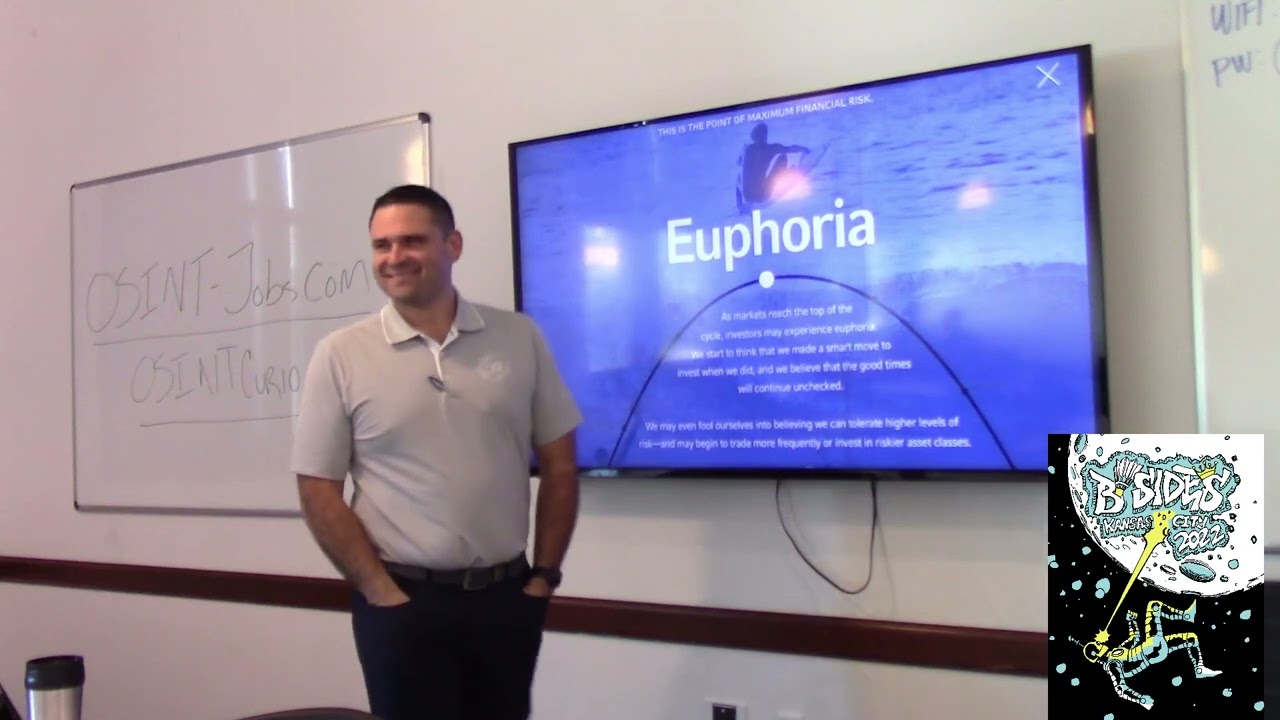

all right so the emotions of investing so as you can see here the blue we talked about optimism excitement thrill euphoria so that Euphoria is where you have the maximum risk that's where everything's going great you think that's that's that's where we're going to be right that's this is never going to come down this is going to be forever that's where you have maximum risk as the market starts to pull back start to see some economic data that's starting to make you wonder what's going on you first tell yourself no it's fine we'll get through it we'll pull through you can go through that denial then you have a little little anxiety you have a little bit of that

what I like to call speaker's stomach little butterflies in there a little bit of that internal like oh what's going on then you get some downright fear like oh should I call my person or should I've gone under my accounts or I've gone on my retirement account should I've gone to cash I've gone to bonds um then the data comes out and the market starts to just come straight down we're really starting to look at it starting to get worried you're starting to panic you're all the way down to the positive that is your opportunity point so I'm going to pause there for a minute has anyone ever heard of it Buy Low sell High raise your hands right

have you ever heard of Buy Low cell why no okay and then the third one I always ask is have you ever heard of buy high sell low one of those three do most people do remember first one second one or third one third absolutely right because your friends your neighbors your buddies like hey I bought Amazon at 800. well now it's worth 2600 you're like what Amazon like I gotta get it today so that's when you buy Hive and all of a sudden it comes down you start selling it right so that maximum opportunity right there is where you really want to get into a market I'm not suggesting nor applying that right now is the throat or the trough or

the lowest point in the market but this is in that point where we're at right now and then you start to come through your little skeptic because the market going to come back and then you hop into some hole get a little bit of relief and guess what if you wash rinse or repeat you start right back over here at optimism what I want to do is I wanted to give you guys a little bit um of just a little education on what I've seen so if you see the market cycle one that's 71 through 75 the second one is 84 through 89. this period right here up until 84 is called stagflation that's where the government did a lot of things

the government did a lot of things and inflation went up the market just saying is for those folks that were around was not a fun time so we have the 97 305 and then as everyone remembers the old uh financial crisis of 05 to 14. now we have Market five which I like to call um is anyone I heard of uh by a relevance biasy right you only remember what happened most recently so we're going to talk about that from 2015 and 2021. so that first part investors have been optimistic excited throwing euphoric in this Mark in the first part of that market in 2015. so I'm gonna give you guys optimism a little definition and this would

typically start with optimism which sits at the inflection point of the emotional upswing the commonly expect this to go our way we expect to have a return of the risk we're investing because we believe that the markets will continue to grow wealth through what we're choosing all right Market cycle five January 15th through February 2020. does anyone know what the most important two points of those dates are month before covid right before the pandemic and then that was on the tail end of the what we call the financial crisis your returns if you had your money in there 79 percent we had full employment in the U.S optimism was just going we had the 2016

uh tax cuts and then trade War really escalated between us and some more foreign continues the cut so when the FED Cuts hit people borrow money cheaply money is in motion business is borrowed to buy build Capital et cetera or build uh inventory out and then we have this little virus that's going to China That's identified we're like you know and I I don't know if you guys have your everyone has their own story but to go to Nashville and uh it was the spring break week our kids we all got together and we got an email make sure your kids take everything home and every teacher is like take it all out taking everything out of your lockers they're

like and then we get the email and as everyone goes everything starts to get shut down those kind of things so um then we start entering in this denial anxious fearful past right we start to wonder about it I'm not going to get through this you understand what fear means but really what what it does is it makes you make a flight to safety you want to go to bonds you want to go to cash those kind of deals so Mark the cycle late February 2020 Market goes down 13 covet starts to hit stock markets fall in late February and then shutdowns are communicated things are starting to get a little you're starting to get a little worried right so you're

having that a little bit of fear a little bit of worry starting to wonder what's going to happen then you start getting to the point where investors are getting depressed Panic they're starting to really worry like what are we doing here what's going to happen and then I apologize and then here it is March 2020 it is officially classified as Global pandemic now we're down 23 percent travel and commerce I'm not sure if there's maybe a handful of jets going around just to take what they call necessary or the folks that had to work and then we're pretty much in a quarantine for two weeks here in the United States some of the world was in

the quarantineers for months right we really got to that point that's that market cycle

and panic at it people were making decisions in their portfolios when I had my clients I had a excuse me I have a roughly 254 clients that I deal with out of all those two sold out most of them I was able to kind of talk at you know hey relax we've been through this before one had to buy a property so I I completely understand what she did what she did the other one sold out and to this day he still saving cash to the spirit now he might have been a genius but maybe he puts that in there now but no one's all this coming so um all right then we start getting that skeptical

hopeful a little bit of relieved we're going to the market going to come back well cares Act was signed we all know about the PPP loan they all know about the things the government did and the market came from March 2020 to December 21. so literally a little over a year and a half they went up 160 percent so if you make cash never got back in you missed out quite a bit probably about 116 relative to what you would own um what I what I really kind of talk about it let me hit that Euphoria right now we're there we're all in and you know this is this is back to where we make Financial

Risk an issue with you because now we're thinking well you know I have all this money I didn't spend during covet Market's pretty high do I jump all in maybe not the question is your time Horizon what kind of emotions can you deal with and the last thing I was so focused is why are you making an investment is it based on the emotions are there items that the conversation you have with people are you making a strategic decision to invest I'll end on this and then this is what um typically I get a lot of well Jimmy when's the best time to invest I say well a couple things one when you have the money

gonna have money do the best two would be are you able to understand what your strategic goal is with it if you're doing it for a short term there are short-term Investments to get into absolutely but what it really ties back into is the third thing can you stomach whatever decision you make and be able to make changes to your goal the last part of our presentation that was on there that Eric and I talked about was do you need a financial advisor or financial planner all those things well

I won't be a little vulnerable and really honest with you all real quick so I've done this for over 10 years I ran Target sword before so I'm well versed in the business world and uh I bought a stock about four years ago um it was a it was kind of a thought I had to go out and research it and found it I bought it at nine dollars a share and I bought quite a bit of it it went to 49.50 and then I thought to myself 50 I'm gonna sell it at fifty dollars right well the next day I got to 50 and a half 50.55 for about three hours and I sat there

I'll make a phone call yeah I sat there well it's still at 15 52. wow and I didn't pull the trigger anyone want to guess what that stock trades at right now take a shot in the dark two days ago I think you did around two dollars now so I needed my own advisor and funny to tell you that taught me enough to know that I have to partner with one of my partners in my firm to say hey when I make a decision a finite decision sell it at 50 help me it's key fact help me put that in the system put it in there for me and I will take my emotions and my thoughts out of

it do you need a financial advisor everyone needs a financial advisor when do you really need one when you have implications of do I know what a Roth is do I know what a traditional area is do I know what I'm doing at work all those questions secondly if you own the business are part of a business there's folks I've met here that are really creates really nice entities if you don't have a CPA or a tax accountant you really need one and then you need to join them with the financial advisor that's the aspect of the point that you need to make good decisions on the legal end and then lastly I would say

everyone most folks I know in the business will always do a 35 45 minute consult and we're really upfront with you sometimes I've told people that weren't my clients yet hey go find one online put it in there start that out make sure you can be a consistent investor and when you get there let's create a financial plan for you so that's really what I talk about when does everyone need a plan or need an advisor I think so because as I said earlier emotions is the part I deal with I'm not a therapist a normal license therapist but I spend half my time in therapy with my clients so as I said I'm Jimmy Gannon I'll open up

the floor to questions and answers and like I said please don't be specific to anything you know related to your account or anything I have to make a recommendation on so questions nothing yeah I know you have a question now go ahead um so in the information security Community there's a lot of healthy skepticism about don't take things at face value that kind of stuff so from a due diligence standpoint picking a financial advisor can feel like a very scary Endeavor so are there things like finra or other kind of due diligence type things that you think are reasonable for people to follow in saying yeah this is a person that I'm willing to kind of make myself

vulnerable with to kind of reach out to me that's a great question thank you so yeah so finra which is our one of our governing bodies um it's one of the financial regulatories there's a little item on there and if you go to any website for an advisor it's we have to legally have this on there's called broker check you click it it should take it you can put in my last name it'll tell you my license they tell you what states I'm licensing at that moment tell you the firms I've worked for and we call disclosures right so if a client had a or even a non-client had a what we call a question or what uh I'm trying to

think the actual word of it but we disclose anything that a complaint even if it's unfounded we would disclose that so my client Mary calls me says things and she has a complaint we will have it on there and investigate it and documented Now read through them don't just see them because some of them believe it or not I've gotten a few Chuckles off of and so someone I know had a they're 18 years old they're on a bike they are young cops we have to put that on there literally it has a whole documentation about how they are around the cops for like 30 miles and eventually pulled over and got arrested it's on there but it's it's

it's disclosed because anything like that has to be on there bankruptcies have to be on there anything else to do legally the last thing I say is don't just do that have a conversation with them I literally rub 20 of the population the wrong way I'm moisturous I'm outgoing I have my hands up I talk I drive my neighbors crazy it's a lot of funny things and so uh just talk to them have a conversation if they're not a good person that's okay they'll probably have someone that's locked opposite of them or most opposite of them and they can connect you uh the last thing is I'll say follow that little thing right here right the gut

you walk in and it just doesn't feel right follow the gut and that's okay I have no problems while having someone walk out of my office because their gut just told them it wasn't thank you for that question because there's quite a few financial advisors and some of them are quite a main form of history about that as well so somebody like Dave Ramsey are they things that you want to keep an eye out for in a good way or how do you how would you separate the two universes um so I'm a little biased on that so and I'll explain why so I work for Lighthouse Financial strategies and for over 15 years we were an EOP

so if anyone doesn't know that that's a local indoor slope endorsed local provider and so Dave talks about that there's a lot of things going on with that I think that's a good place to start um but I wouldn't necessarily put all my eggs in that and say that person's great because the I think what we talked about earlier is a part of it and also take take for granted just because someone recommends them you don't always know what goes on in the back end how that recommendation came by or even if it's endorsed or however you want to call it where that came from um but if your advisor or future advisors talking to you they just can't

betrayed with you that kind of answers and there should be a conversation about anything I'll answer 95 of anything a few things personal matches per person you talked about the company and how did you researched it before you invested into do you have any kind of tips on how to go about researching and picking different companies yeah um so I I would call myself a little bit of a stock jockey on stocks mutual funds I have a portfolio meter that works in our office that handles all my mutual fund trades I just there's 8 000 mutual funds or actually more than that but there's 8 000 that we could use on our platform after that's

too much so that but individual stocks yeah so uh cash balance sheets fundamentals um truly understanding what the executive teams do and that's by no means a recommendation that's just some ideas they're going to look at all their things are on K1 so they put them all online on the SEC they have to file a recorder and you can actually see what the executive office is doing if they're buying selling the last thing I would probably tell you is this is really simple and but look around and while you spend your money or your friends and family and people around you spend your money right so if they're spending their money there I always say this Walmart's

parking lot never seems to be empty is that a good stock bad stock I don't know we can dig into it more but it's a good place to start all the things around I just see apple I see you know I can look around and see all Samsungs I can see all these different things out here that we use every day that's one of my things too I have to be able to understand what they produce or what their service think about thank you put your thoughts on index funds uh so I'm going to give you a very uh very simple thing everyone loves them when they're going up because I can't beat the index because it's the index

right and some of my accounts have fees and I'm telling my accounts have Commissions in them so it's very difficult to feedback um everyone hates somebody goes down because you ride the index now so what we call up capture down capture what your portfolios has a 90 up capture you're getting 90 of that index down capture you want to try to do that the other way and only capture you know 50 of it because then because then that's where you make your crew your crop right the one thing I will tell you is the indexes change to the sides of the companies sometimes the company's in there for the wrong reasons they've gotten so many stocks purchased

they've gotten so much volume that they are in that S P 500 for the wrong reason and you don't want to be a part of that one company which holds 20 of that agency so passive Management's fine there's no nothing wrong with it I just don't care for it because I'd rather pay people to help me manage mutual funds and and do that because I the way I think of it is I'm not sure if anything is worse for you I don't know if I'd answered your question and if you're going to do index funds make sure your advisor doesn't throw a one and a half percent fee on there because that just doesn't make sense but

that that's out there the world but I don't get it and I don't speak for anyone sitting across in a different picture so you don't make really do a whole bunch you know useful fun here you have somebody else manage it for you yeah who would like who am I believing for just as an Indian smoker um you mean for me my virtually or well we have a portfolio manager in our office and his job is to manage hundreds of millions of dollars for us that's his job to sit there and make decisions based on it and not all the money's in there you know there's the movie the new insurance and individual stocks he doesn't do stocks because there's

there's a lot of companies I do them because I enjoy them I have a conversation with you about it um but in the end it typically goes back to he understands the mutual fund he jumps on the calls he talks to their portfolio managers so we make a selected choice in our office to have someone manage and handle that yeah so most people are here today to get smarter on information security network and so on and and you're not here expecting this new financial principles anymore than we'd expect you to get information security professional but uh it seems like part of your Notch stick but part of your you know the value in having those

conversations for us of our financial IQ online below so my question to you is are there things that we should be would be in our interest to kind of be uh spending a little time maybe of course will give them a week if there's one or two places for us to start to level up our you know kind of financial IQ and other suggestions yeah other than your newsletters yeah no no no no I mean you could talk to me after this but I made a it's an artist told the organization I'm not here to teach me I'm here to educate but uh so I would tell you that the one or two sticky note things you need to do

by Tuesday is find out if your company actually does a retirement plan hey B do they Mash and see are you even in it because sometimes you're automatically enrolled and you have no idea and you're like oh yeah I get this email from Prudential I have no idea what that is but I just move on because I'm busy so that's one right do that two is uh this is hard for everyone locate your last three months of spending and truly understand what you spend and what's coming in if that number is consistently negative you got a problem just be dead honest with you and you're using the emotions somewhere in there to avoid it to one

day it's going to give you anxiety and it's going to blow up again so um the the third thing I would tell you is if for any reason none of it makes sense call someone ask a friend if they have one ask you know just go talk to anyone that you know that has an advisor and have a conversation what that relationship looks like because I will tell you right now I've had clients come in here and tell coming to me and tell me the most audacious things that their spouse may not even know about but they forgot to tell me about an account for two years I'm not quite sure how you're going to

tell me you buried a body in your backyard but then you forgot that you had that Ameritrade account finances are so personal we get very you know there's emotions deal with it there's some embarrassments and before you there's all these things with it just be straight find someone to help you out with most advisor will have a conversation with you it's just it's that simple so stupid husbands fight over that a lot very much now um they've probably heard it before so the embarrassment fact is you know it's very personal but you're not the first person and you probably won't be able to yeah and the way I look at it is I get it I don't hold it against anybody but

much like any professional doctor lawyer if you kind of don't give me all the information best you can we might make some decisions together that that do more harm than good time um yeah just two things one earn the hard way and bust early time earns money number two Insurance get it while your inmates sounds stupid but if the chief was pretty good uh you know while you're young because you'll pay less you'll be over if you don't want to have a conversation with the insurance there's two types permanent and turned I'm in the betterment village all day um you can Google it Believe It or Not There are two different types one one you definitely need for sure lock it in

one you have an option depending on how you feel about investing and if someone has entered some instruments and been guided into some instruments early in my career and had to learn as I went you know it's it's it's just like security since you're you know it's part of your lifelong learning yeah oh I mean the plan changes we can do a plan and you're going to save eight percent every year you're gonna you know retire with seven million dollars and then you have kids or then you get ill or you switch jobs or something like that all of a sudden you can't do it it's like every year it's like a doctor when you just go in there we do look at

the plan is it going to work no what can we do to change it and are you okay with the outcome every year that's what I do with my clients a minimum of once a year we talk well thank you all I appreciate it very much thanks for excellent [Applause]

Related talks

47:57

47:57 1:04:24

1:04:24 33:07

33:07 34:22

34:22 27:53

27:53 50:11

50:11